Interchange Fees and the True Cost of Running a Parking Payment System

Every time a driver taps a card at a pay station, a set of fees flows silently through the payment network — before a single dollar reaches the operator’s bank account. For facilities running a modern parking payment system, these costs are unavoidable, but they are far from uniform. Interchange rates vary by card type, transaction method, and even how the card data is captured. Operators who understand the mechanics end up paying measurably less than those who treat their monthly processing statement as an inscrutable utility bill.

This guide breaks down each layer of payment cost, explains how the Durbin Amendment changed the calculus for debit cards, and walks through the statement forensics that routinely uncover hundreds or thousands of dollars in unnecessary fees.

The Three-Tier Payment Cost Stack

Every card transaction processed through a parking payment system passes through three distinct cost layers. Conflating them is the most common mistake operators make when evaluating processor proposals.

1. Interchange

Interchange is the fee paid to the card-issuing bank — the institution that gave the driver their Visa or Mastercard. It is set by the card networks, not by your payment processor, and it is non-negotiable at the individual merchant level. Interchange is expressed as a percentage of the transaction plus a flat per-transaction cent amount (e.g., 1.51% + $0.10). The full published schedules are publicly available: Visa posts its U.S. interchange reimbursement fee schedule and Mastercard publishes its merchant rate document. Reviewing these directly is worth the effort — the schedules are dense but they tell you exactly what category your transactions should qualify for.

2. Assessments

Assessments are fees paid directly to the card networks (Visa, Mastercard, Discover, Amex). They fund network infrastructure and brand operations. Assessment rates are small — typically 0.13% to 0.15% — but they apply to every transaction regardless of card type. Like interchange, assessments are non-negotiable. What varies is whether your processor passes them through at cost or bundles them into a blended rate that obscures the true markup.

3. Processor Markup

This is the only layer where negotiation is possible. Processor markup is how payment companies make money — it sits on top of interchange and assessments and can take the form of a flat percentage, a per-transaction fee, monthly minimums, or a combination. In an interchange-plus pricing model (also called cost-plus), the markup is separated out clearly on your statement. In a tiered or flat-rate model, it is blended in, often at a significant premium.

Understanding which model your parking payment system contract uses is the single most important step before any cost reduction conversation.

Credit vs. Debit Interchange for Parking Payment Systems

Not all cards are equal from a cost perspective, and the gap between credit and debit interchange is substantial. A standard Visa consumer credit card transaction might carry interchange of 1.51% + $0.10 under the CPS/Retail category. A signature debit transaction on the same Visa-branded card often runs closer to 0.80% + $0.15. PIN debit — where the driver enters a four-digit code — is typically cheaper still, often under 0.50% + $0.15.

For a parking payment system that processes thousands of low-dollar transactions daily, the distribution of credit versus debit cards in your transaction mix has a meaningful impact on blended effective rate. Facilities in urban markets with a high share of daily commuters tend to see more debit card usage than airport or event parking, where expense-account credit cards dominate. Knowing your own mix — broken out by card type — is basic operating intelligence that many operators lack because their processor statements obscure it.

One important note on Visa and Mastercard debit: the card may look identical to a credit card, but the interchange category is entirely different. If your payment terminal or pay station is not correctly identifying card type at the point of sale, you may be paying credit interchange rates on debit transactions. This mis-categorization is more common than it should be and is worth auditing with your processor.

Durbin Amendment and Regulated Debit

The Durbin Amendment, enacted as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act, fundamentally changed debit interchange economics for merchants. The Federal Reserve implements the amendment through Regulation II, which caps interchange on debit transactions issued by banks with more than $10 billion in assets at $0.21 + 0.05% of the transaction, with a potential fraud-adjustment addition of $0.01.

In practice, this means that when a driver uses a debit card issued by a large bank — Chase, Bank of America, Wells Fargo, and most major issuers qualify — the interchange the parking operator pays is capped at roughly $0.22 to $0.24 per transaction regardless of transaction size. For a $6 parking transaction, that cap is highly favorable. Without it, uncapped debit interchange on a percentage basis would represent a larger share of a small ticket.

However, the Durbin cap does not apply to debit cards from banks with under $10 billion in assets — so-called “exempt” issuers. Credit unions, community banks, and smaller regional institutions are exempt, meaning their debit cards may carry higher interchange. In practice, the majority of consumer debit volume flows through large issuers, so most parking operators benefit from the cap on the bulk of their debit transactions.

Operators should also understand that Durbin requires card networks to offer merchants a choice of at least two unaffiliated networks for debit routing. This network-routing rule allows merchants to choose the lower-cost network for each debit transaction. Whether your payment terminal and processor are configured to take advantage of least-cost routing is a legitimate question to raise in your next processor conversation.

Card-Present vs. Card-Not-Present at Pay Stations

The physical interaction between a card and a payment terminal defines the card-present versus card-not-present distinction — and it has direct interchange implications for every parking payment system.

Card-present transactions, where a chip card is dipped, a contactless card or mobile wallet is tapped, or a magnetic stripe is swiped, qualify for lower interchange rates because the physical card authentication reduces fraud risk. Card-not-present transactions — where a driver enters card details manually into a web interface or mobile app without a physical reader — are treated as higher risk and carry a premium, typically 0.3% to 0.5% higher than the equivalent card-present category.

This matters because many operators run parallel acceptance channels: an attended or unattended pay station (card-present) alongside a mobile payment app or web-pay option (card-not-present). When a customer pays via the mobile app, every transaction is card-not-present. Depending on volume, the differential adds up. For mobile parking payment solutions, operators should factor this into their total cost modeling rather than evaluating the payment channel purely on customer experience and technology benefits.

Contactless EMV — tap-to-pay via physical card or mobile wallet — qualifies for card-present interchange rates and also reduces transaction time at the pay station, which has its own operational benefits. Ensuring your hardware supports and actively promotes contactless acceptance is both a cost and throughput optimization.

How Transaction Size Impacts Parking Economics

Parking is structurally challenging for payment economics because transaction sizes are small. A $5 garage ticket, a $3 meter feed, or a $2 short-stay payment creates a disproportionate per-transaction fee burden compared to a $50 retail purchase. The flat-cent component of interchange ($0.10 per transaction, for example) hits small tickets far harder in percentage terms.

Some card networks have historically offered small-ticket interchange programs — reduced percentage rates with no or minimal flat per-transaction fee — for merchants whose average transaction falls below a defined threshold. Visa and Mastercard both publish small-ticket categories in their interchange schedules. Whether a parking merchant qualifies depends on average ticket size, merchant category code (MCC), and whether the processor is correctly submitting transactions to optimize for the applicable category.

Parking operators are typically coded under MCC 7523 (automobile parking lots and garages). Ensuring your MCC is correct matters because some interchange categories are MCC-specific. An incorrect MCC — sometimes assigned during merchant boarding and never revisited — can result in systematically higher interchange than you should be paying.

For facilities running a high volume of micro-transactions (under $3), the economics of card acceptance can become genuinely problematic. Some operators in this range explore alternative approaches covered in the surcharging section below.

Negotiating With Payment Processors as a Parking Operator

Payment processors expect negotiation from sophisticated merchants. The leverage points available to a parking operator are not identical to those available to a retailer, but they exist.

Volume is the primary lever. Processors price risk and administrative cost against transaction volume. A multi-facility operator processing $2 million annually has meaningfully more leverage than a single-lot operator. If you have multiple facilities with separate merchant accounts, consolidating to a single processing relationship often unlocks better pricing than each account would receive independently.

Pricing model matters more than headline rate. Migrating from a tiered pricing model to interchange-plus is almost always beneficial for operators who have the scale to negotiate it. Under interchange-plus, you pay the actual interchange cost plus a disclosed, fixed markup. Under tiered pricing, the processor assigns each transaction to a “qualified,” “mid-qualified,” or “non-qualified” tier — and the non-qualified bucket, where rewards cards and corporate cards often land, can be priced at 3%+ with no transparency into the underlying interchange.

Contract terms deserve scrutiny. Monthly minimums, PCI compliance fees, batch fees, statement fees, and early termination penalties all contribute to total cost. A seemingly competitive processing rate paired with a $50/month PCI fee and a $500 early termination penalty on a multi-year contract can easily be worse than a slightly higher rate with no ancillary fees.

When requesting proposals, ask each processor to provide a sample monthly statement format and a fee schedule that itemizes every charge. Processors who resist this transparency should be treated with appropriate skepticism.

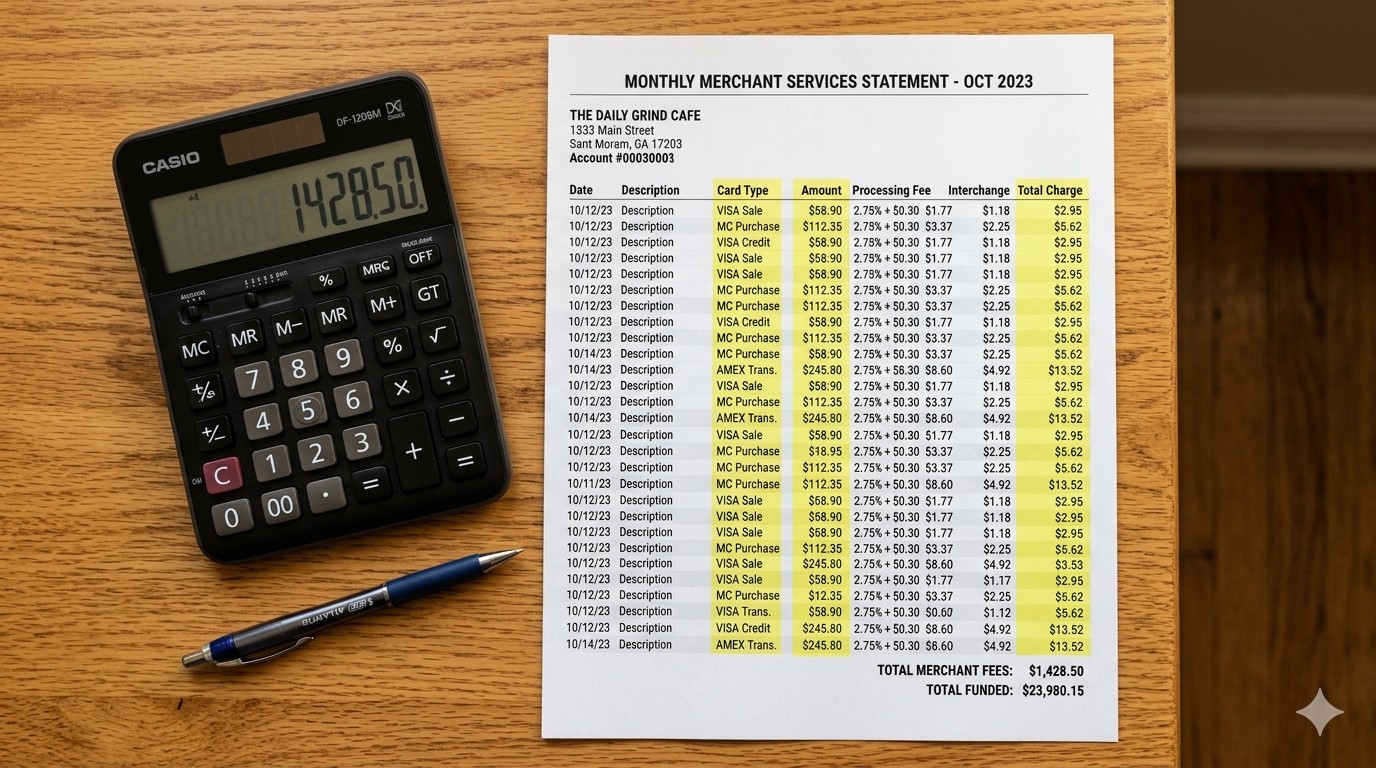

Monthly Statement Forensics: Finding Junk Fees

A processor statement for a parking payment system can run several pages and contain line items that most operators have never scrutinized. Below are the categories most likely to contain unnecessary costs.

Network fees passed at a markup. Assessments and network access fees should appear on your statement at cost. If your processor is adding margin to these pass-through items, it is a signal that other costs may be inflated as well.

Downgrades. When a transaction fails to qualify for the standard interchange category — due to incomplete data submission, batch settlement delays, or card type — it downgrades to a higher-cost category. Chronic downgrades indicate a data quality or configuration problem with your payment terminal or point-of-sale system. A high downgrade rate is fixable, but only if you know it exists.

Duplicate or unclear fees. Regulatory fees, network access fees, and compliance fees sometimes appear under multiple line items that represent overlapping costs. Comparing your statement against your processing agreement is the only way to identify these.

PCI non-compliance surcharges. Processors are permitted to charge a monthly fee for merchants who have not completed their annual PCI DSS self-assessment questionnaire. These fees range from $20 to $50 per month. Completing the SAQ eliminates them. For further context on reconciling these costs with your broader revenue picture, see our guide on parking revenue reconciliation.

A useful benchmark: a well-run parking operation on interchange-plus pricing should have an effective rate (total processing costs divided by total volume) between 1.8% and 2.4% depending on card mix. If your effective rate is consistently above 2.5%, something warrants investigation.

When to Consider Surcharging or Convenience Fees

Surcharging — adding a fee to credit card transactions to recover interchange costs — is legal in most U.S. states following card network rule changes, but it comes with strict compliance requirements and carries genuine customer experience risk. The rules are not simple.

Under Visa and Mastercard rules, a merchant who surcharges must notify the network in advance, display clear signage at the point of entry and the point of sale, cap the surcharge at the operator’s actual cost of acceptance (not to exceed 3%), and apply the surcharge only to credit cards — not debit. Applying a surcharge to debit transactions violates network rules.

Convenience fees are a related but distinct concept. A convenience fee is charged when a customer uses a payment channel that is not the merchant’s standard acceptance method. An operator who primarily accepts cash at attended booths and offers an online pre-pay option could charge a convenience fee on the online channel. Convenience fees are not subject to the same cost-cap requirements as surcharges but are restricted to the alternative channel — you cannot apply a convenience fee at a pay station where card is the primary payment method.

From a practical standpoint, surcharging in parking is uncommon except in specific contexts: high-volume facilities where card mix skews heavily toward premium rewards cards, or operators who have a substantial cash-paying customer base and want to avoid penalizing cash customers. The customer experience friction and operational complexity of a surcharge program typically outweigh the cost savings for mid-size operators.

Cash discount programs — where card-paying customers see the full price and cash customers see a discounted price — are legally distinct from surcharges in most states and may offer an alternative approach, but they require careful structuring to comply with both state law and network rules.

Further Reading

The foundational documents for understanding interchange are the publicly published rate schedules maintained by the card networks. Visa’s current U.S. interchange reimbursement fees and Mastercard’s merchant rates document are updated periodically and are the authoritative source for any interchange category question.

For regulatory context on debit interchange caps and the Durbin Amendment, the Federal Reserve’s Regulation II overview explains the implementation rules and the current cap structure in plain language.

For additional context on how these costs fit into the broader architecture of a parking payment system, see our overview of how parking payment systems work. Operators managing multiple payment channels — including mobile — should also review our coverage of mobile parking payment economics, where card-not-present rate differentials have a compounding effect on total processing cost.